You know that from time to time I am fond of bank cards, cashbacks and conversion rates. As a result of my research, I wrote a post Bank cards for travel, in which he told me what cards I myself have and which ones can be made. Of course, the list is incomplete, there are much more cards, but based on personal experience, besides, I am updating it, as I keep track of tariffs.

Recently, questions about Alfabank cards have become more frequent, and with them the matter is murky. Therefore, I asked Alfabank's technical support about fees, made myself Alfabank cards, and checked everything in practice. But in order not to write only about one Alfabank, I conducted an experiment with all my cards at once..

The content of the article

- one Alfabank's answer about the conversion rate

- 2 Which of the 6 bank cards is more profitable

- 3 conclusions

Alfabank's answer about the conversion rate

I recommend Tinkoff AllAirlines card with cashback up to 10% for booking, 3% for tickets and 2% for all purchases. Read my post Pros and cons of the card.

All Airlines card (1000 rubles as a gift)>

The fact is that when shopping abroad with Alfabank cards, there is a 2.5% commission, which is advertised in few places, and it does not always arise. They wrote to me several times in the comments that, they say, there are no commissions. But in order to say this for sure, you need to know all the nuances. Before describing the results of my experiment, I offer you an answer from Alfabank's technical support, where it says in black and white about a 2.5% commission. I quote.

In accordance with the Bank's Tariffs, for cash withdrawal through third-party ATMs (except for partner banks) a commission of 1% of the amount is charged, including the commission of a third-party bank, but not less than 180 rubles. for Service Package «Optimum». We recommend to clarify the availability and size of the commission of a third-party bank in its support service..

We would like to note that when performing a transaction in a currency other than the currency of the account to which the card was issued, with the use of which the corresponding transaction was performed, the Bank converts into the account currency in the manner and under the conditions provided for in Appendix 4 - «General conditions for the issue, maintenance and use of cards» Of the agreement.

Three currencies are always involved in the conversion process: transaction currency, billing currency and card account currency.

Operation currency - the currency in which the operation is performed using a bank card (cash withdrawal, payment at a point of sale or transfer from card to card).

Billing currency - the currency in which the international payment system calculates the amount to be debited from the cardholder's account. The billing currency for VISA and MasterCard payment system cards for transactions in foreign currency abroad is US dollars..

Account currency - the currency in which the account is opened, to which «tied» the card with which the transaction is performed.

If the currency of the Client's account differs from the transaction currency and billing currency, then the conversion will be carried out according to the rules and rate of the payment system (MPS) from the transaction currency to the billing currency, and at the Bank's rate from the billing currency to the account currency. In accordance with the rules of the IPS, the Bank has the right to apply correction factors to the base rate of the IPS. For Alfa-Bank cards, the ratio is 2.5% (except for VISA Infinite and MasterCard World Signia / MasterCard World Elite cards, which are converted without applying a correction coefficient). This information is recorded in the documents regulating the mutual settlements of the Ministry of Railways and the Bank, and can be changed. Thus, the conversion from the transaction currency to the billing currency occurs at the rate set in accordance with the rules of the IPS, which allow applying correction factors to the base rate. The course of the MPS can be found on the MPS website. This course is for informational purposes, since at the time of the operation there may be one course, and at the time of authorization of the operation - another. When converting from the billing currency to the account currency, the Alfa-Bank rate is applied, which the Bank has the right to set at its discretion.

In this case, the following rule applies at Alfa-Bank: if the transaction currency coincides with the currency of the Client's account, then the amount debited from the Client's account will be equal to the amount of the transaction.

Just in case, I will summarize the entire answer of the technical support. If you withdraw dollars from a dollar card, or from a euro euro, then there will be no 2.5% commission. If you withdraw baht, shekels, zlotys and other tugriks from currency cards, or you withdraw something from ruble cards, there will be a 2.5% commission, except for holders of VISA Infinite or MasterCard World Signia / Elite cards.

Which of the 6 bank cards is more profitable

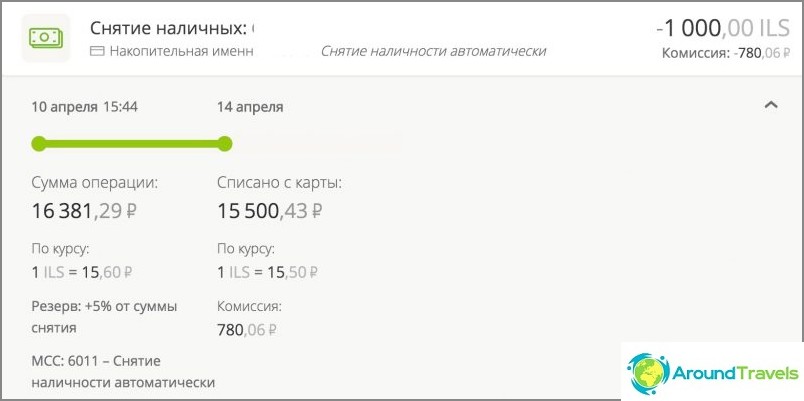

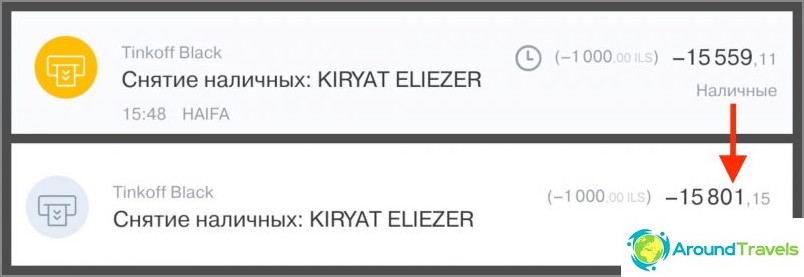

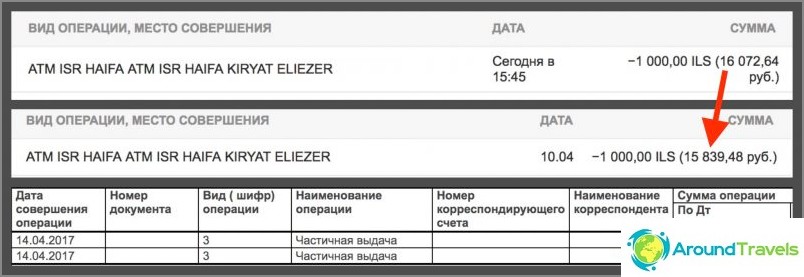

As I said above, I decided to conduct an experiment with all the cards that I have with me at once: Tinkoff ruble and dollar, Corn with a connected interest on the balance, Sberbank Mastercard, Alpha ruble and dollar. I withdrawn from the same ATM, the same amount of 1000 shekels, at the same time on April 10, 2017 with a difference of several minutes.

Let me remind you that there were 2 conversions on ruble cards (ILS => USD => RUB): the first (ILS => USD) is carried out by the Mastercard or Visa payment system, the second (USD => RUB) is carried out by a Russian bank. For dollar cards, there was only 1 conversion (ILS => USD), which is carried out by the payment system, and the rate of the Russian bank in this case is not involved, but nevertheless it can charge its commission. For Thai baht, there would be exactly the same scheme.

You also need to understand that although the authorization of funds (withdrawal from an ATM) was at the same time, then their real withdrawal occurs after 2-5 days and at the rate on the day of withdrawal. Accordingly, the conversion rates and the final amounts (which we compare) are different, and because of this, too (the rates change at least once a day). I will separately say about dollar cards - it is important at what rate the dollars were bought, if we compare which is more profitable than the ruble or dollar cards (about this I somehow wrote a whole post). For example, they can be bought in advance at one of the rate drops, in the Internet bank immediately before withdrawing from an ATM, or in an exchanger on any day..

Authorization Withdrawal Withdrawal fee Total withdrawn Note Maize Mastercard World 16381.29 15500.43 0 15500.43 Withdrawal after 3.5 days. There is a bug in the IB and the commission is displayed. After the write-off, this line should disappear, but the bug has not yet been fixed. When the service is connected «Percentage on balance» up to 50 thousand rubles per month withdrawal from ATMs without commission, then 1%. Tinkoff Black ruble 15559.11 15801.15 0 15801.15 Write-off after 3 days. There is no commission for withdrawal from ATMs within 150 thousand rubles / month. Sberbank Mastercard ruble 16072.64 15839.48 158.39 15997.87 Write-off after 3 days. The commission for withdrawing from an ATM (1%) is not displayed anywhere in the IB, although it is debited immediately. You can see her only in a full statement in the IB, after about 5 days, not everyone knows this. Alfabank ruble 16293.33 15899.47 180 16079.47 Write-off in 4.5 days. The commission for withdrawing from an ATM (1%) is displayed in the IB in a separate line. Tinkoff Black USD $ 276.33 $ 273.85 0 $ 273.85 Write-off after 3 days. No ATM withdrawal fees up to $ 5,000 / month. Alfabank dollar $ 284.08 $ 280.70 3.18 $ 283.88 Write-off in 4.5 days. Commission for withdrawal from ATM (1%) is displayed in IB in a separate line.

Withdrawal by card Kukuruza

Withdrawal with Tinkoff ruble card

Withdrawal on the ruble card of Sberbank

Withdrawal with Alfabank ruble card

Withdrawal with a Tinkoff dollar card

Withdrawal with Alfabank's dollar card

conclusions

The most common advice on the banking forum is Corn for rubles, and Tinkoff Black for currency, if we're talking about travel. And this basically coincides with my advice, as well as with the results of the experiment. Although I am more for a currency card (more profitable) and for an AllAirlines travel credit card with a 2-10% cashback (according to the link 1000 rubles per card as a gift).

At first I wanted to recalculate all the courses-numbers with a calculator, but the picture is exactly the same as it should be according to the tariffs, so I decided that just a free plate with the amounts would be enough.

First of all, this experiment can be useful for those for whom, the phrase «on the XXX card as much as 4% of the commission» does not mean anything, and who does not want to understand all these courses. Agree, when you give specific amounts, especially in comparison, it is clearer than some kind of percentage. Indeed, in fact, the difference between the cards when withdrawing is only a few hundred rubles. Not everyone will want to bother and make special, slightly more profitable cards because of such a difference, especially if there are only one or two trips a year..

Another thing is those who like to count money, or who use cards abroad throughout the year. You see, it is much more pleasant not to give the bank a commission, but to receive cashbacks from it back. And, the more you spend per year, the greater the difference. For example, I save on annual maintenance, on conversion fees, at the expense of cashback, say, 15 thousand rubles per year. Is it a lot or a little? If you consider this as work, then it is not enough, if you consider money from nowhere that I get, poking around in the topic that I like, then a very pleasant bonus. It should be noted that I figured out the issue and made maps a couple of years ago, that is, I have not been sitting day and night reading forums for a long time, no. Also, if you take the amount of not 15 thousand rubles, but for example 150 thousand rubles, 200 rubles of the difference already turns into 2,000 rubles. Well, and so on, you yourself can multiply (for 1.5 million rubles there will be a difference of 20,000 rubles).

Therefore, I recommend everyone to approach the choice of bank cards with their heads. If you don't really need a bonus, then it's easier not to bother yourself and make almost any card. If you want to get everything from the bank, you will have to read the tariffs and choose something specifically for yourself.

P.S. Questions? 🙂